What is salary sacrifice for pension contributions and how does it currently work?

Salary sacrifice is an arrangement where employees agree to reduce their entitlement to cash pay in return for a non-cash benefit (in this case, an equal amount of employer pension contributions).

Salary sacrifice schemes can be used for other types of benefits as well, though the proposed cap would only apply to pensions, not other uses such as childcare or cycle-to-work schemes.

Salary sacrifice for pension contributions effectively makes them free of both employee and employer NICs (because it swaps pay, which is subject to employee and employer NICs, for an employer pension contribution which is not).

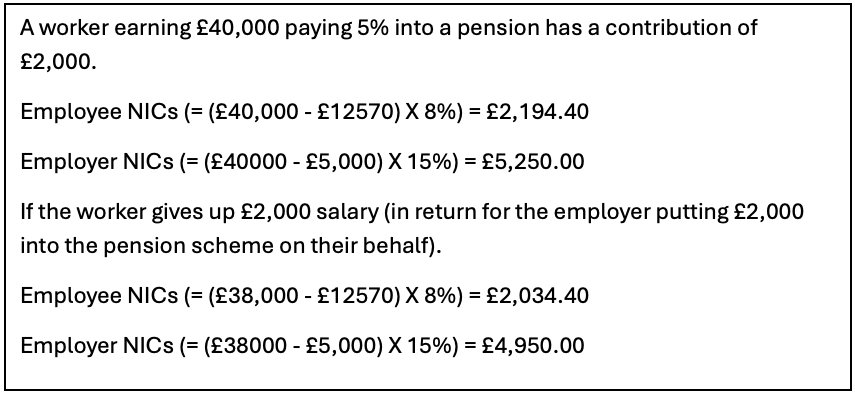

An example can illustrate this:

The employee NIC saving usually results in an increase in take-home pay of the same amount. The employer NIC saving can accrue entirely to the employer or is sometimes shared with the worker in the form of an additional employer pension contribution.

Is it a good idea to use salary sacrifice for pension contributions

We cannot provide financial advice.

The employee NIC savings from contributing through salary sacrifice are illustrated by the example above.

Note that the savings are not as significant for higher earning employees because their marginal NIC rate is 2%.

Sometimes employees get a direct share of the employer NIC savings. But the indirect benefit can be more important, the savings could enable the employer to increase pay.

There are certain technical issues that must be allowed for to ensure that salary sacrifice schemes do not have unintended detrimental impacts.

For example:

- Pay rises should be based on pre-sacrifice salary.

- Employers should provide pre-sacrifice salary information to mortgage brokers and providers.

- Care should be taken that eligibility for certain National Insurance benefits are not affected.

Please contact your local representative or full-time official for support on an existing scheme or a proposal to introduce one.

Who uses salary sacrifice for pension contributions

There are some issues with the data on the use of salary sacrifice, so published information may not be completely accurate.

Data from 2019 suggested that 30% of private sector employees and 9% of public sector employees used salary sacrifice.

This seems broadly consistent with HMRC’s impact assessment suggesting 7.7 million employees working for 290,000 employers used salary sacrifice for pension contributions.

Survey data suggests that larger employers are more likely to use it.

Prospect does not hold data on the use of salary sacrifice by specific employers, if your employer operates salary sacrifice, but you have not previously seen an update about this issue, please ask your full-time official (to check whether they are included on our new list of employers who operate salary sacrifice schemes.

How this measure would limit the use of salary sacrifice for pension contributions

As stated in Treasury guidance: from April 2029, only the first £2,000 of employee pension contributions through salary sacrifice each year will be exempt from NICs.

Employers and employees can still make contributions above £2,000 through salary sacrifice arrangements.

However, employee contributions above this amount will be subject to employer and employee NICs like other employee workplace pension contributions.

Contributions through salary sacrifice, like all pension contributions, will still be exempt from Income Tax (subject to the usual limits).

There are some details about implementation that will probably not be clear until formal consultation periods open:

- NICs apply on a pay period basis, but the cap appears to be annual. Will there be a pay period cap that is equivalent to £2,000 annually?

- Will someone employed for part of the year have a £2,000 cap for that or one that is pro-rata’d?

- When someone changes job mid-year, how will their new employer know how much headroom is available against the cap?

- NICs apply on a per job basis, but the cap appears to be per individual. How will employers share headroom against the cap where someone has two or more jobs?

What the impact of the measure would be on workers and employers

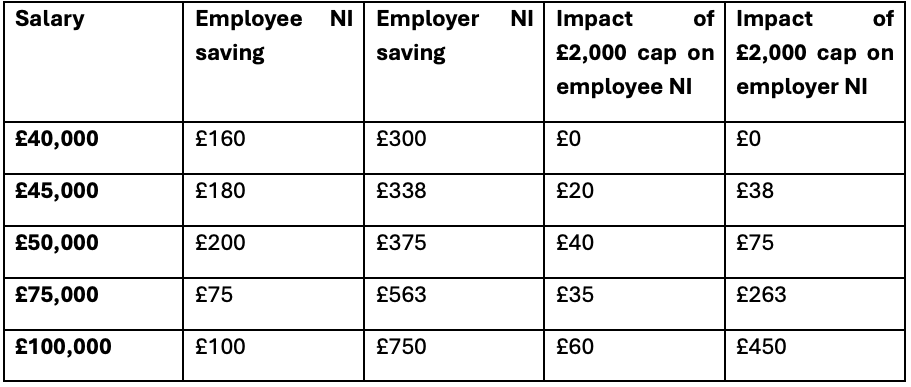

The table below shows the impact a £2,000 cap would have on the basis of the current NI thresholds and rates where the member contribution rate is 5%.

This table shows the measure starts impacting members earning £40,000 a year or more

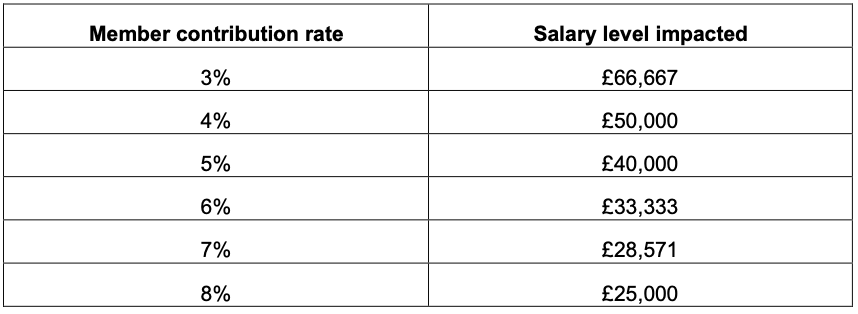

The table below shows the earnings level at which the measure starts to impact members for a given level of member contribution rate.

The prooised cap has much more impact on employer NICs than employee NICs. However, most of this cost will be passed onto employees.

How will the measure be implemented

The government has already introduced primary legislation that would give it the power to cap the amount of salary sacrificed pension contributions exempt from NICs by regulation.

Some commentary suggested that the speed with which the legislation was brought forward was related to a desire to convince financial markets about its resolve to raise this money.

Once the Bill receives Royal Assent, the government would subsequently consult about, and then lay, regulations implementing the proposed cap.

What Prospect is doing to lobby Parliament about this

Prospect issued briefings for MPs ahead of the second reading and committee stages of the Bill in the Commons.

We also wrote to members of branches that we were aware had members in salary sacrifice schemes. More than 1,000 members used our tool to write to their MP about it.

We will write to the Minister and provide further briefings to Parliament as the Bill progresses through Parliament.

There should be further opportunity to make representations about this policy, if and when regulations are subject to consultation in the future.

Working with employers to mitigate the impact of the measure

There will be much common ground between Prospect and employers on the issue of restricting the benefits of salary sacrifice. We will work with employers about this wherever possible.

Prospect officials have also started engaging with employers about steps that could be taken to mitigate the impact of the cap if it was introduced.